Why Did My Credit Score Drop? 11 Reasons

If your credit score dropped overnight, don't panic. Review these possible causes behind your credit score's fall, and score-boosting steps to take next.

Reviewed by: Adam Liebich, BECU Credit Bureau Usage Manager

If your credit score dips, it could be a short-term response to something like a new credit card application. Or it could be something with longer lasting effects, like an old bill going to collections.

Consumers worry their future credit application will be rejected, according to 2023 research by the New York Federal Reserve. Almost one third of consumers didn't apply for, or were turned down for, some credit at least once in 2023, according to the Consumer Financial Protection Bureau.

At the same time, the average credit score has increased dramatically over the past 13 years, according to credit bureau Experian. The average score in 2023 is 715, up from 689 in 2010.

If you're wondering why your score dropped for no reason, and you need to apply for credit, don't panic. Here are potential reasons for a credit score drop, examples of how it happens and what you can do to reverse the trend.

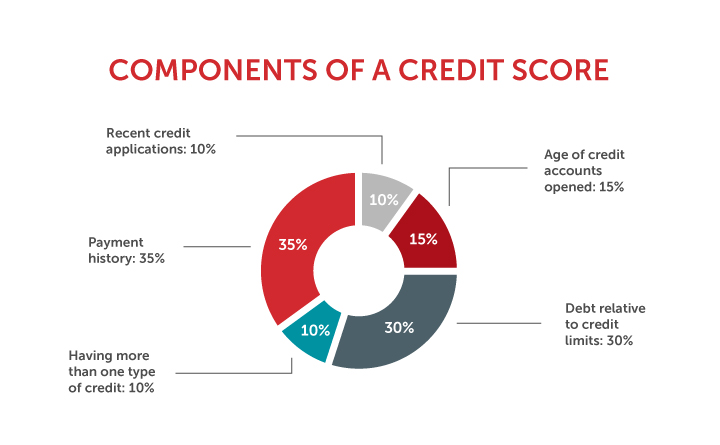

Although there are several types of credit scores, we'll focus on the FICO score because it's the score commonly used by the top U.S. lenders to estimate their risk if they lend you money.

1. You Made Late Payments

Your payment history makes up 35% of your credit score — the biggest piece of your score's pie. Most creditors, such as your credit card company, report missed payments to three credit bureaus (Experian, Equifax and TransUnion) at these intervals:

- 30 days (about one month)

- 60 days (about 2 months)

- 90 days (about 3 months)

- 120 days (about 4 months)

- 150 days (about 5 months)

Example: You missed two payments on an infrequently used credit card. Creditors report late payments to the credit bureaus, and your score drops due to the negative information on your credit report.

What to do: Set up automatic payments for your credit cards and loans, if you can, to ensure on-time payments. If you're struggling financially, speak with your creditor immediately. See if you can create a payment plan that won't hurt your credit score.

2. You Opened a New Card

The average age of your credit makes up 10% of your credit score. Older credit increases your score, while new credit decreases your score.

In addition, the credit issuer will make a hard inquiry when you apply for a new credit line. Hard inquiries can cause your score to drop roughly five points. Multiple hard inquiries for new cards within a short time can rapidly reduce your score.

Example: You apply for three travel cards through different issuers but aren't approved. You now have three hard inquiries on your credit history, which lowers your score by 15 points for about one year. The brand-new credit card reduces your credit's average age and trims your score.

What to do: Don't apply for credit impulsively. Once you're approved for a new credit card, don't apply for more cards until your score recovers from the newly added account and the hard inquiry. FICO credit scores only consider inquiries within the past 12 months.

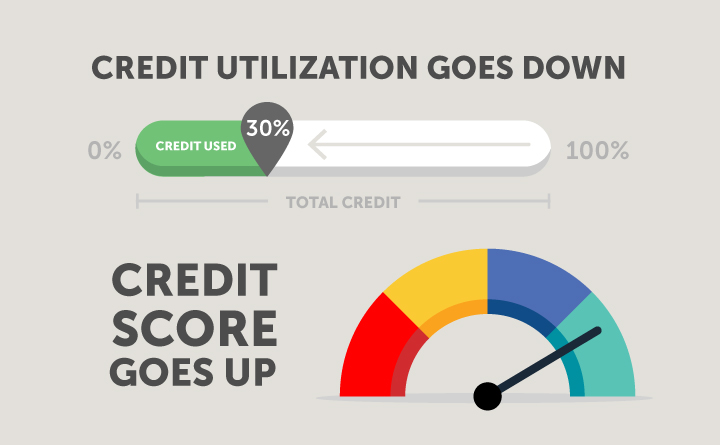

3. You Have a High Balance

Your credit utilization ratio is the amount of credit you're using today out of all the available credit you can access. A higher credit score goes to those who keep their credit utilization ratio under 30%.

To find your credit utilization ratio, divide your total outstanding debt by your total credit limit.

Example: Suppose you have credit cards with limits of $5,000, $10,000 and $7,000 for a total of $22,000 available credit. You spend $10,000 total in December. Divide $10,000 by $22,000 to discover you're using 45% of your credit.

What to do: Make regular monthly payments until your credit utilization ratio is below 30%. In this example, that means getting your balance below $6,600.

4. You Paid Off an Installment Loan

"Credit mix" makes up 10% of credit scores, and only having one account type could temporarily lower your score. Two account types make up your credit mix:

- Installment loans: A loan repaid regularly in installments, including student loans, personal loans, mortgages and car loans.

- Revolving credit accounts: This type includes credit cards and HELOCs. Your balance owed goes up and down as you repay.

Example: You paid off your auto loan, which caused your score to drop because it was your only installment loan. The rest of your accounts are revolving accounts.

What to do: Don't get another installment loan right away to bump your credit score or diversify your credit mix. Apply for a mortgage, personal loan or car loan when you're ready and your owed amounts are low.

5. You Closed an Account

Closing a credit card account could lower your credit score. You've probably reduced the amount of credit available to you, which changed your credit utilization ratio.

Example: Suppose you had three credit cards with limits of $5,000, $10,000 and $7,000. Combined, you have $22,000 available for spending. You decide to close the credit card with the $7,000 limit. Now, you only have $15,000 in available credit.

What to do: If you have more than one card with an issuer, ask the issuer to transfer the credit limit of the card you want to close to another card. This will boost your credit limit increase on your existing card. If you have a card you aren't using, but haven't yet closed, review your credit report frequently to ensure someone else isn't using it.

6. You're an Identity Theft Victim

Your credit score might drop if someone uses your identity to apply for credit cards, a mortgage or other loans.

A fraudster could trigger hard inquiries due to card applications, late payments or high credit card balances if a card is successfully acquired. All can lower your credit score.

Example: You notice your credit score dropped significantly in one month. You check your credit history with the credit bureau and discover that your account lists several cards you've never had, adding to your debt on record.

What to do: First, order your credit report from the three bureaus to see if someone has been applying for or using credit in your name. Then, follow the government's advice at IdentityTheft.gov. Steps may include adding a fraud alert to your account so no one can open new accounts in your name.

7. You Filed for Bankruptcy

Bankruptcy offers a fresh start for borrowers looking to get relief from debt payments but could affect your credit score by up to 200 points, according to research from FICO. Bankruptcies can stay on your credit report for up to 10 years.

Example: You can no longer pay your debt and you file for personal bankruptcy. Your credit score plummets drastically.

What to do: Meet with a credit counselor to discuss strategies to rebuild your credit or discuss options with your bankruptcy attorney.

8. You Were Unable to Pay Your Mortgage

If you're having problems paying your mortgage, it will likely decrease your credit score. Issues could include:

- Late payments: You pay your mortgage more than 30 days after the due date.

- Short sale: You sell a house for less than you owe the bank and can't pay back the difference.

- Foreclosure: You can no longer pay your mortgage and the bank repossesses the home.

Among these issues, the smallest decrease in your credit score generally results from late payments of 60 to 90 days, which could drop your score by 80-100 points, according to FICO. Short sales and foreclosures lead to greater credit score decreases, dropping a score by 100 points or more.

Example: You fell behind on mortgage payments by four months. You discover a major credit score drop when next checking your credit.

What to do: Time helps credit scores recover, as long as you prevent adding new debts or late payments to your credit report. However, it could take as long as seven years to recover from a foreclosure. Speak with your lender to avoid mortgage delinquencies.

9. Your Car Was Repossessed

Repossessions happen when you don't make loan payments toward an asset such as a car. Repossessions stay on your credit report for up to seven years.

Example: You got behind on car payments by more than 60 days after a job loss, and the lender repossessed your car. When you next apply for credit, you realize your credit score dropped due to a combination of factors, including late payments and loan default.

What to do: Try to avoid repossession by negotiating with your lender. You may be able to pause payments or otherwise modify your payment plan. If repossession has already occurred, begin exploring strategies to pay any future creditors on time and rebuild your credit.

10. A Bill Went to Collections or Charge-Off

If a creditor goes unpaid for 120-180 days, a creditor could "charge off" the debt, which means it has given up on collecting it. However, that charge-off will go onto your record for up to seven years, regardless of whether you end up paying it. The creditor can also send your unpaid debt to collections, which will also stay on your record for up to seven years.

Example: Your credit score drops, so you review your credit report and see a bill you'd ignored. You see that the creditor has now charged off your debt, and the debt has been sold to a collection company.

What to do: Contact the original lender or the collection agency to negotiate a payment plan or settlement.

11. Your Credit Report Contains Mistakes

If your credit score drops and none of the above reasons apply, know that credit report mistakes could drag down your score. FICO depends on your credit history to determine your credit score. Common credit report mistakes include:

- Closed credit accounts reported as open.

- Credit accounts incorrectly reported as late.

- The same debt listed more than once.

- Incorrect credit card balance or credit limits.

- Incorrect delinquency dates or other negative information.

Example: You review your credit report and notice your student loan is listed twice, which makes it look like you have more debt than you carry. This leads to a lower credit score.

What to do: Follow the CFPB's advice for disputing errors on your credit reports, including disputing with the company that provided the information and the major credit bureaus.

Myths About Credit Score Drops

Your credit score won't drop due to:

- Tax liens: Legal claims made against your property for unpaid taxes, which the three credit bureaus stopped collecting in 2017, according to the CFPB.

- Lawsuit judgment: The three credit bureaus stopped collecting judgments in 2017, including public records such as lawsuit judgments, civil judgments and unsatisfied judgments.

- Checking your credit score: You can check your credit score as often as you wish without hurting it.

- Employer inquiries: Like checking your own score, an employer inquiry won't ding your score.

In some cases, there can be nuance, too. Suppose you submit multiple applications over a month as you rate-shop for a home or auto loan. These applications won't lower your score the same way as if you applied for multiple credit cards in one month.

And some negative information may be reported by credit bureaus in some situations — for example, if you're applying for a high-income job or a significant amount of life insurance. However, this won't lower your credit score.

Credit Score Frequently Asked Questions (FAQs)

What is a good credit score?

For most lenders, anything above 700 is considered good to very good and should help qualify you for a mortgage or car loan.

Why did my credit score decrease for no reason?

Your credit score is based on information included on your credit report. Your score may drop because of changes or errors in your report, or because your credit card balance was much higher last month. Payment history, debt and length of credit history all contribute to your score. If you notice a sudden drop, check your credit report for any errors.

How long does a credit score drop last?

According to research from FICO, the time it takes to recover depends on what led to the credit score drop and your starting score. For people with higher credit scores, it take longer (five to seven years) to recover after a drop due to a serious event (such as bankruptcy or foreclosure). For those with lower scores, recovery ranges from nine months to five years.

Credit Reporting Agency Help

If you explore all these potential causes for a decrease in your credit score and you still need help understanding what's going on with your credit, you can reach out to the credit reporting agencies. They work directly with consumers on changes to credit information and might be able to answer your questions.

The above article is intended to provide generalized financial information designed to educate a broad segment of the public; it does not give personalized financial, tax, investment, legal, or other business and professional advice. Before taking any action, you should always seek the assistance of a professional who knows your particular situation when making financial, legal, tax, investment, or any other business and professional decisions that affect you and/or your business.

Related Content

Lora Shinn

Contributor