How To Use Secured Credit Cards To Build Credit

Combined with on-time debt payments and low credit utilization, secured credit cards can help you build a strong credit history to help raise your credit score.

With good credit comes lower interest rates on your debt and better odds of getting approved for auto loans, credit cards and housing rentals.

But where do you start if you have no credit history or your credit score is low?

If you're a college student, young adult, new to the U.S. or you're recovering from a financial setback, a secured credit card might be a good option for you.

Secured credit cards work like a normal credit card for purchases. What secures your card is the refundable deposit you pay that acts as collateral for your charges.

"A secured card is a great starter card to build your credit," said Jeffrey Kim, Director of BECU's Credit Card Product Strategy.

Secured credit cards can help you build the three largest contributors to credit scoring: Payment history, amounts owed and length of credit history.

With consistent, timely payments and keeping your debt low, you can build a strong credit history and raise your credit score, increasing the likelihood that you'll qualify for a traditional, unsecured credit card.

You may also become eligible for a higher credit limit than your initial deposit.

10 Steps To Build Credit With a Secured Credit Card

1. Pay the Required Security Deposit

Secured credit cards require a minimum refundable deposit of your own money in an account. This amount varies by financial institution, ranging from a few hundred to several thousand dollars. BECU's secured credit card, for example, has a $250 minimum and $10,000 maximum deposit and depends on the amount you're approved for.

If you can deposit more than the minimum, you'll increase the limit on your secured credit card, giving you more flexibility in spending.

2. Regularly Use Your Secured Credit Card

You won't be able to build your credit history if you don't use your card, so don't stash your secured credit card in a drawer. Instead, use it throughout the month for small amounts that you know you can afford to pay back.

Your bank or credit union reports your monthly charges and payments to the three major consumer credit bureaus: Equifax, Experian and TransUnion. This history helps raise your credit score.

3. Stick With One Secured Credit Card

It is best to apply for just one secured card. Make purchases with this card regularly and pay on time until you've built up a good credit payment history.

Opening too many credit card accounts within a year can lower your credit score. The length of credit history makes up 15% of your FICO score — the credit score most often used by credit unions, banks and lenders in evaluating applications for credit.

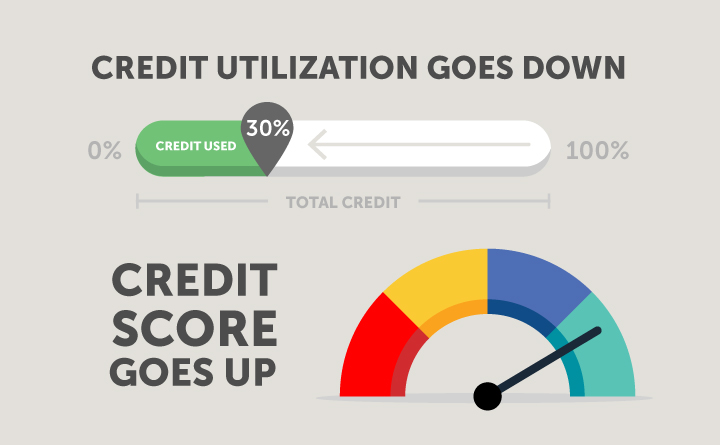

4. Mind Your Credit Utilization Rate

Only use a portion of your available credit and keep your balance low. In general, stay under 30% of your credit limit. This is good practice for your future credit use.

You'll get a higher FICO score if you keep your total credit use (all loans and cards) under this. The amounts owed in total makes up 30% of your credit score.

Example: If you deposited $1,000 as your security deposit, keep your balance to less than $300. If you have a $100 security deposit, keep your balance to less than $30.

5. Never Max Out Your Secured Card

You never want to max out your card except in an emergency.

"If you're new to using a credit card, it can be easy to over-spend and reach your limit. The debt can add up fast," Kim said. "Don't think about your secured credit card as 'free money.' Think about your spending in the context of how much you can pay back."

6. Review Your Spending and Budget

Learn to review your spending every month when your statement arrives by mail or online. Ensure all the transactions shown are the correct amount and no unauthorized purchases were made.

7. Make Monthly Payments On Time

Every month, pay at least the minimum required payment — or more — by the due date to avoid paying fees. This on-time payment is reported to the credit bureaus.

The largest contributing factor to your FICO credit score is your payment history, which makes up 35% of your score.

You can't rely on your security deposit for any missed payments.

"Best practice is to pay off the full balance," Kim said. "The whole purpose of a secured card is to get into the habit of using your card and making a payment. A pattern of consistent payments helps improve your credit score. So, we encourage our members to pay back as much as they use."

8. Don't Miss a Payment

A missed payment on your secured credit card could lead to a late fee and interest charges.

The card issuer will report missed payments to credit bureaus, likely bringing down your credit score. If necessary, set up an automatic payment process to deduct the minimum payment from your checking account before the date due.

9. Review Your Credit Score

The credit card issuer providing you with a secured credit card will likely give you free credit score access and updates. Review this score monthly and learn how it changes based on your credit use. Over time, you should be able to watch as your credit score improves.

10. Review Your Credit History

Once a year, you can access a free credit report from the major consumer credit bureaus. Review this history and make sure it's accurate. Promptly report any errors that could impact your credit, such as misspelled names, accounts that don't belong to you, or signs of identity theft.

How Long Does It Take To Improve Credit With a Secured Credit Card?

Building a strong enough credit history to qualify for an unsecured credit card is not an overnight process. Suppose you have no credit history or limited credit history. In that case, it may take 6-12 months of consistent credit-building habits (such as on time payments) to establish credit and achieve a good credit score. Then, you may qualify for traditional, unsecured credit cards.

If you have a credit history and a low credit score, repairing your credit typically takes much longer — sometimes years. You may not qualify for a traditional credit card if you have late payments on other debts, delinquencies, charge-offs or property repossession.

In those cases, you may need a more detailed strategy to rebuild credit. Consider consulting with a free credit and debt counseling service such as GreenPath if you need to repair your credit.

Choose the Right Secured Credit Card To Build Credit

To find the best secured credit card for the purpose of building credit, make sure it meets the following characteristics before you apply:

- Card use and payments are reported to the three credit bureaus.

- No annual fees to have and use the card.

- Low interest rate — or you can pay off the card in full every month.

- Security deposit earns interest while you're building credit.

- Financial institution offers an appealing unsecured credit card to which you can "graduate."

Not all secured cards are the same. Some may have a very low credit limit or don't offer a rewards program, so be sure to review the details before you apply.

Approval subject to BECU membership, credit approval and other underwriting criteria; not every applicant will qualify. Credit Card programs, services, rates, terms and conditions are subject to change without notice. Contact BECU for the most current information.

The above article is intended to provide generalized financial information designed to educate a broad segment of the public; it does not give personalized financial, tax, investment, legal, or other business and professional advice. Before taking any action, you should always seek the assistance of a professional who knows your particular situation when making financial, legal, tax, investment, or any other business and professional decisions that affect you and/or your business.

Related Content

Lora Shinn

Contributor