Are CDs Worth It Right Now?

If you don't need access to your money right away, a CD might be a good savings tool for you in 2024 while average interest rates remain high.

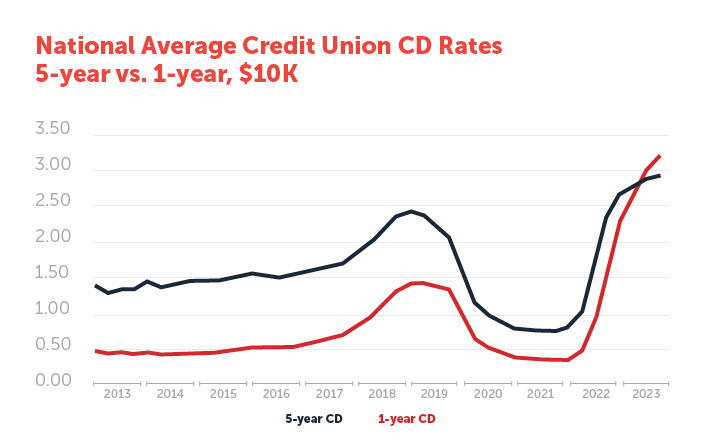

CD interest rates are high in 2024 — higher nationally, on average, than they've been in more than a decade, according to Forbes Advisor.

But great rates aren't the only thing to consider when trying to help your money grow. Sure, if you open a traditional CD now, you'll lock in your rate for the term of the CD, but you'll also lock up your money for that term.*

Whether a CD is worth it right now also depends on why you're saving money, how soon you need your funds and whether rates rise or fall in the next year or five years.

"In my opinion, right now is a great time to get a CD," said Scott Smith, head of BECU's deposit product strategy. Smith has served the credit union industry for 22 years. "But no one has a reliable crystal ball."

He explained that financial institutions consider potential moves by the Federal Reserve when determining rates. The Federal Reserve's lending rate "tells us the direction CDs are going."

It can be challenging to time the market and snap up the perfect savings tool at the perfect moment. We'll help you weigh the potential pros and cons of CD investing right now.

Why CD Rates are High in 2024

Right now, you may find higher-rate CDs with terms of just a few months.

Historically, long-term CDs — defined as 18 months or more — have been more likely to have higher rates than short-term CDs. For example, BECU's highest CD interest rate is on 12-month to 17-month CDs (at the time of publication). In 2024 and for the past year or so, Smith explained that we're in an "inverted yield curve," where the situation is reversed. Short-term CDs have higher rates than long-term CDs.

Higher short-term rates suggest that many banks and credit unions expect the Federal Reserve to start cutting rates in June 2024. If so, financial institutions are likely to protect against paying interest on high-rate CDs long-term, after rates fall.

Often, these inverted yield curves can also indicate a future recession.

"A more normal yield curve helps create a stable rate environment with more predictable returns for members," Smith said.

How Do Current CD Rates Compare With the Expected Rate of Inflation?

As of March 2024, inflation over the past 12 months is about 3.2%, according to the Bureau of Labor Statistics Consumer Price Index. The average credit union CD rates are slightly lower or equal to inflation, according to the National Credit Union Administration. However, you can find CD rates featuring interest higher than inflation.

Fed chair Jerome Powell has indicated a target inflation percentage of 2% must be reached before the Fed will feel comfortable lowering their rates, Smith said. There's a widespread expectation that rates will lower in 2024 as inflation's peak seems to be subsiding and meeting Powell's requirements.

However, financial institutions want to retain the deposits, so CD rates may stay higher in 2024 — just slightly reduced by the end of the year. "Hence, that's why right now is the best time to consider a CD to lock in the presumed 'peak' of the market," Smith said.

CD Investing Pros and Cons in 2024

CDs can be a smart financial move at times, but not so great at others. In the past, other investments earned higher rates than even the best CDs could earn. But, in today's high-interest-rate environment, CDs might be a great option. Here are the pros and cons of CD investing in 2024.

Pros of CD Investing Right Now

- High current rates: CD rates are comparatively high right now, especially on shorter term lengths. For example, a one-year CD at a credit union earned 0.95% interest on average in the fourth quarter of 2020. But it earned 3.2% interest on average in the fourth quarter of 2023, according to the National Credit Union Administration.**

- Good time for CD newbies: In 2024, you should be able to find high-rate CDs for one to 12 months. As a result, you won't lock up money long-term and can learn more about choosing, opening and rolling over a CD (or withdrawing your funds).

- Stable rates on opened CDs: Stocks and bonds have had a bumpy few years with dramatic highs and lows. Fixed-rate CDs pay stable returns no matter the overall economy's fluctuations.

- Interest rates may start declining soon: CD returns could also start declining if the Fed begins lowering interest rates. The window for opening a higher-rate CD before rates decline may be closing.

Cons of CD Investing Right Now

- Risk of opportunity cost: If your money is locked up in a CD, you can't put it into a potentially higher-interest opportunity, such as a recovering stock market, without early-withdrawal penalties.

- Risk of potential rate increases: CD rates may have peaked. But if CD rates continue going up for some reason, most banks and credit unions won't increase your rate unless you have a bump-up or step-up CD.

- Multiple accounts to manage: Opening high-interest-earning CDs at different banks and credit unions can create a hassle of tracking CDs. A forgotten CD may be automatically rolled over into the exact term you had — even if rates are lower.

Are CDs Worth It When Rates Are Rising?

In general, a CD is worth it if rates are rising, and you can easily find and open a CD with a higher interest rate than a savings account. In the current inverted yield curve, short-term CDs will usually have a higher rate, and those CDs may be a good option.

But if CD rates continue to go up, you could miss out on a higher rate in the future by locking in funds now. Some investors deal with this by investing in bump-up CDs, which offer the opportunity to increase their rate if CD rates go up.

You can also manage rising-rate risk by putting money into CDs in staggered intervals.

Example: Imagine you have $1,000 to save but worry that rates may increase. You could put in $500 in a six-month CD now. If you notice rates go up a few months later, you can put your remaining $500 in another six-month CD.**

Are CDs Worth It When Rates Are Dropping?

If rates drop, you may feel pressured to snag a higher-rate CD interest before the rate is gone. A CD of any term will maintain the same returns when interest rates drop.

As a historical example, you could have opened a five-year CD in 2019 at 2.06% interest (the average rate at that time). But if you waited a few months — until March 2020 — to open your CD, rates had already dropped to 1.56% for the same CD. You'd miss out on hundreds of dollars worth of earnings by waiting just a few months to open the CD.

Here's how it would affect earnings if you invested $10,000, with interest compounding monthly:**

| Interest Rate** | Earnings after five years | |

|---|---|---|

| Five-year CD in December 2019 |

2.06%

|

$1,083.94

|

| Five-year CD in March 2020 |

1.56%

|

$810.68

|

In an inverted yield, as we're experiencing now in 2024, a shorter-term CD may be a good option. Short-term rates are higher on average. If rates continue to drop and if the CD environment returns to normal, longer-term CDs will feature higher interest rates than short-term CDs. At that time, longer-term CDs may be more worthwhile.

Is a CD Ladder a Good Strategy Right Now?

When rates are high and falling in 2024, a CD ladder strategy may not be the best option, Smith said. This is because a CD ladder strategy assumes longer-term CD interest rates are higher than shorter-term CD interest rates. Or the CD ladder strategy may assume rates will stay about the same or even go higher over time.

When Might a CD Not Be Worth It?

A CD might not be worth it if you need your money soon, such as within a few weeks, and you don't have emergency funds to rely on. You'll pay a penalty for closing the account early and lose your excellent interest rate. Opening a CD account also may not be worth it if the financial institution charges an early withdrawal fee.

Can You Lose Money on a CD?

You could lose several months of earned interest if you withdraw funds early from a CD. However, you probably won't lose your principal (the original amount you deposited). But read the fine print — a bank or credit union's penalty for early withdrawal could lead to losing some principal you put into the CD.

Is Putting Money in CDs Safe Right Now?

CDs are among the safest investments you can make with your savings. These accounts are insured by FDIC (if a bank) or NCUA (if a credit union) up to $250,000. As a deposit account, a CD is more like a very safe savings account, not an account with stocks or bonds you could lose money on.

How Are CD Rates Determined?

The Federal Reserve sets a benchmark federal funds rate — basically, the target rate for financial institutions to borrow and lend each other money. This short-term interest rate has increased dramatically in the past few years to slow down inflation. In total, the Federal Reserve raised rates 11 times in 15 months.

Although these rates don't directly set CD interest rates, they do influence them. So, CD rates have also risen significantly over the past few years. Other interest rates, including those for credit cards, mortgages and savings accounts, have also risen significantly.

Inflation has cooled somewhat (PDF) since last year, according to a recent Federal Reserve report, and the Federal Reserve stopped raising interest rates in June 2023. So, there may be indications that CDs are at their peak earning potential right now.

The Takeaway: Are CDs Worth It Right Now?

Opening a CD in 2024 may be a good idea if you think CD rates will drop in the next 12-24 months. It could pay off to lock in your interest rate before rates drop.

However, finding a long-term CD (such as five years) that competes with shorter-term CDs (such as three months) could be challenging. It's also possible that if inflation becomes challenging again, the Fed could resume raising rates. Carefully consider your savings goals and be willing to adjust strategies if the economic climate changes in 2024.

* Member Share, Member Advantage, or Early Saver savings account required to establish membership; not everyone will qualify. An early withdrawal penalty may apply. Fees will reduce earnings.

**Where examples are used, the products, rates and returns are not guaranteed and are for educational purposes only. The information and examples are not advice and may not reflect the rates, products, or services currently available from BECU. BECU does not offer or guarantee products or rates in this article.

The above article is intended to provide generalized financial information designed to educate a broad segment of the public; it does not give personalized financial, tax, investment, legal, or other business and professional advice. Before taking any action, you should always seek the assistance of a professional who knows your particular situation when making financial, legal, tax, investment, or any other business and professional decisions that affect you and/or your business.

Related Content

Lora Shinn

Contributor