11 New Year Financial Resolutions for 2025

Make financial resolutions you can stick to and learn the specific actions you can take to achieve each one.

Stacey Black

(She/Her/Hers)

BECU Lead Financial Educator

Updated Dec 16, 2024 in:

Budgeting

New Year's resolutions often focus on physical health, but financial health is important, too.

Financial Resolution Essentials

Ideally, New Year's financial resolutions focus on your desired goals and outcomes. Resolutions might include budgeting, saving for emergencies and reducing debt. The key to any resolution is making sure you can stick to it. An "approach-oriented" goal is more motivating and successful for resolution-makers than an avoidance-oriented goal, research shows.

Approach-oriented goals involve achieving desired goals and outcomes. Avoidance-oriented goals focus on avoiding undesirable outcomes. An example of an approach-oriented goal would be committing to paying down debt according to a debt-reduction strategy you choose. An avoidance-oriented goal would be just to get out of debt.

With that in mind, we put together a list of approach-oriented financial New Year's resolutions and actions that can help you improve your financial life. Work your way through our recommended personal finance actions, and by the end of the year, you'll be closer to achieving your financial goals.

1. Resolution: Start a Budget (or Fine-Tune My Budget)

Action: Choose a Budget Strategy

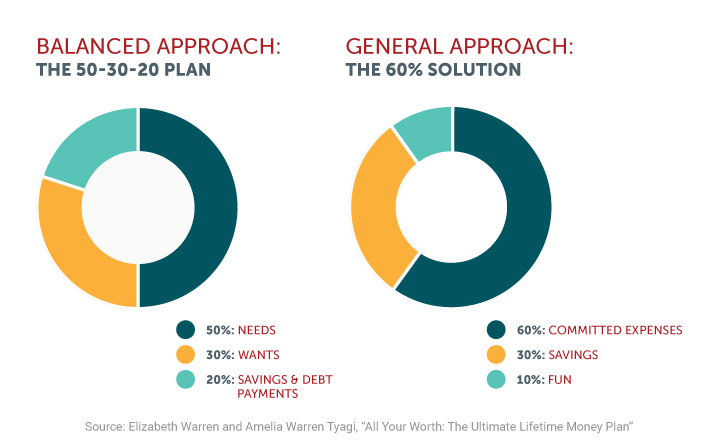

Maybe you prefer a general approach, like the 60% solution, where you reserve 60% of your money for committed expenses, 30% for savings and 10% for fun.

Or maybe the 50/30/20 budget plan is your style — 50% for needs, 30% for wants and 20% for savings and debt.

Remember that budgeting doesn't have to be perfect, and you can change strategies if the one you choose isn't working for you.

Get started by understanding your spending habits. Look back at where you spent money the past few months and track your current spending with a spending journal. Compare your outgoing money to your income.

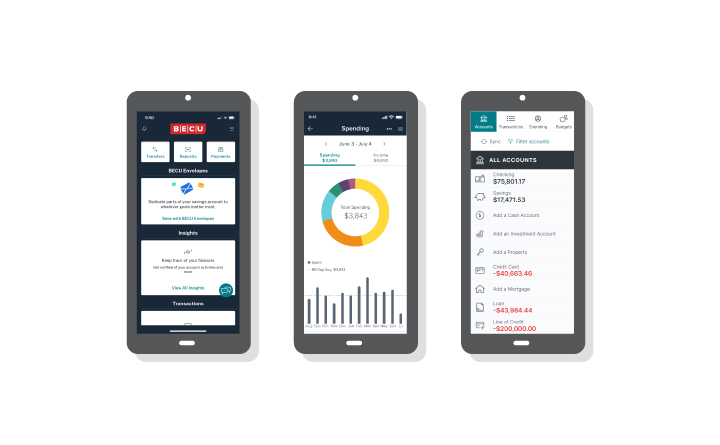

BECU's Better Budgeting tool is one helpful resource.

Budgeting Apps

Budgeting apps can help you track your spending and progress toward goals. The easy-to-use budgeting app Mint was discontinued — but BECU's free Money Manager might be a great alternative. There are many others to choose from, as well.

Research what works for you. You want to end each month knowing where your money went and not feel surprised or overwhelmed when you check your account balances. Also, keep in mind, there are ways to budget while considering inflation.

2. Resolution: Build My Emergency Fund

Action: Create an Automatic Savings Transfer

Your emergency fund helps when the unexpected happens — whether that's new medical bills, fixing your car or being laid off. If you have a financial safety net, you won't need to run up credit card debt and end up paying interest.

As a general rule of thumb, your emergency fund should contain three to six months' worth of living expenses. Make sure you put your growing stash of cash in FDIC- or NCUA-insured savings accounts.

Set up an automatic savings transfer that sends cash to the account with every paycheck or once monthly. It's okay to start small and increase amounts as you go.

BECU members can also explore Save-Up, the automated savings tool that lets you build savings by using your debit card.

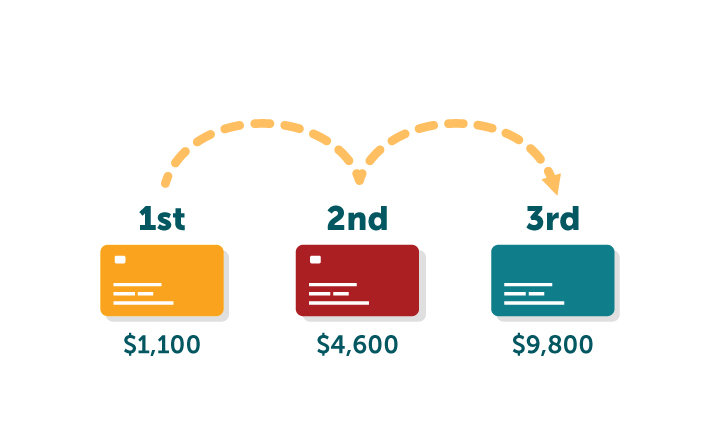

3. Resolution: Reduce My Debt

Action: List Debts and Choose a Strategy to Repay Them

Debt can affect your life in many ways, including whether you will be approved for a personal loan, credit card or mortgage, and the interest rate you will pay.

Paying interest monthly also depletes the cash for saving and spending on things you enjoy.

Add up your total debts, including:

- Credit cards

- Student loans

- Auto and other vehicle loans

- Mortgages and HELOCs

- Medical debt

Review your total debt amount and investigate different methods for paying it down: debt snowball, debt avalanche or debt cascade. There isn't a one-size-fits-all solution. Choose the strategy that is most motivating to you.

If you find it challenging to take this step, BECU members can make a free Financial Health Check appointment.

4. Resolution: Save for My Big 2025 Expenses

Action: Start Saving for Recurring and Occasional Expense

The start of a new year is an excellent time to review significant expenses that happen every year. Instead of relying on credit when these expenses pop up, start saving for them now as part of your monthly budget.

Large annual expenses you might plan for include:

- Holidays

- Birthdays

- Vacations

- Taxes

- Insurance payments

- Donations

Look through 2024's expenses to get an idea of how much you might spend on the same expenses in 2025. Divide the estimated total by 12 to see how much you should save monthly and make this part of your budget.

Consider opening a separate account to keep these funds secure and to help avoid the temptation of spending the money on something else. You can also categorize your savings with our digital tool, BECU Envelopes. Set up automatic transfers each month so you know the money will be here when you need it.

You'll also want to estimate the cost of big purchases you plan to make in the next few years such as buying a car, paying for college or relocating, and start saving for them now.

When it comes to stashing these funds, compare different savings options, focusing on their interest rates to determine the best way to grow your money. For example, a certificate of deposit (CD) typically offers a higher interest rate than a savings account, but requires you to lock in your cash for a set period of time.

5. Resolution: Find Better Interest Rates on Credit Cards and Loans

Action: Compare Rates on Credit Cards, Mortgages and Other Loans Before You Apply

Interest rates, in general, have been climbing, so the new year is a good time to review. You may be paying too much for your borrowed money, particularly if you haven't checked rates in a while.

Credit unions generally offer interest rates that are lower than the average rates found at banks.

You can also look into consolidating your debts with a lower-interest personal loan or find a credit card with more competitive rates — but do so with caution. Debt consolidation can seem like an easy fix, but if you don't make changes to your spending and saving habits, it could end up causing more harm than good. Make sure you've addressed the behaviors that got you into debt in the first place and that you can cover all of your expenses without adding more debt.

For homeowners, if you purchased your home with a higher rate, refinancing may provide a great opportunity to benefit from a lower mortgage interest rate and save you money over the long term. Be sure to weigh the pros and cons, however, as refinancing can also come with upfront costs.

6. Resolution: Improve My Credit Score

Action: Check Your Score Once a Month

The first step to improving your credit score is checking your score. An excellent credit score can help you get better rates on loans.

Credit card companies, lenders and financial institutions often share credit scores with their customers. BECU members, for example, can check their FICO® credit scores for free by logging into their accounts online.

Checking your credit score once a month or so is a good idea — as is understanding why your score might go up or why your score might drop. Different factors influence your ever-changing credit score.

Watching your credit score change and improve can encourage your efforts, and checking your own credit score or credit report doesn't lower your credit score. Although they don't provide a free credit score, you can use annualcreditreport.com to get your credit reports for free.

- Make on-time payments

- Reduce credit card balances

- Limit new credit accounts

7. Resolution: Update My Retirement Plan

Action: Check Retirement Balances and Make an Appointment for a Check-Up

Are you on track for retirement? Total your retirement balances in IRAs, 401(k)s, projected Social Security benefits and pension funds. You can use free online retirement planning tools like the U.S. Department of Labor's worksheet, which estimates how much you should save.

For a more thorough check-up, consider making an appointment with a personal financial advisor to review your strategy. Your advisor can help update you on what's new in 2025 and share new ways to save. For example, those 50 and older at the end of the calendar year can put extra money into retirement annually, through "Catch-Up Contributions."

8. Resolution: Plan for a Future Home Purchase (or Remodel)

Action: Estimate Purchase or Construction Costs and Compare Loan Options

Whether you want a new house or just a new kitchen, you likely know that home purchases and updates are expensive. With some planning, you can take advantage of tax deductions, government programs and better interest rates.

If it's your first time buying a home, research any first-time homebuyer programs available to you and compare requirements and costs.

Energy-efficient upgrades may qualify you for tax credits if you decide to remodel or update your current home.

If you're considering using a home equity loan or personal line of credit to pay for these updates, make sure to compare features, rates and terms when choosing the best option.

Overall, credit unions generally offer lower interest rates than banks for home mortgage refinancing, HELOCs, and home improvement loans.

9. Resolution: Start (or Update) My Estate Plan

Action: Review and Update Bank Account Beneficiaries

Your estate is the property you leave behind after passing away. You don't have to be wealthy to have an estate. It can simply be what's in your checking, CD and savings accounts, or any retirement or pension accounts.

List and review your accounts as a first step. Check who the beneficiaries are on each account — the people you've named to receive your account funds after you pass away. This is a good idea especially if you've encountered any big life changes in the past year such as a marriage, birth, death or divorce.

You may need to complete paperwork or an online form to update the recipients.

If you're ready to learn more, start delving into estate planning with a professional — including how wills and trusts work.

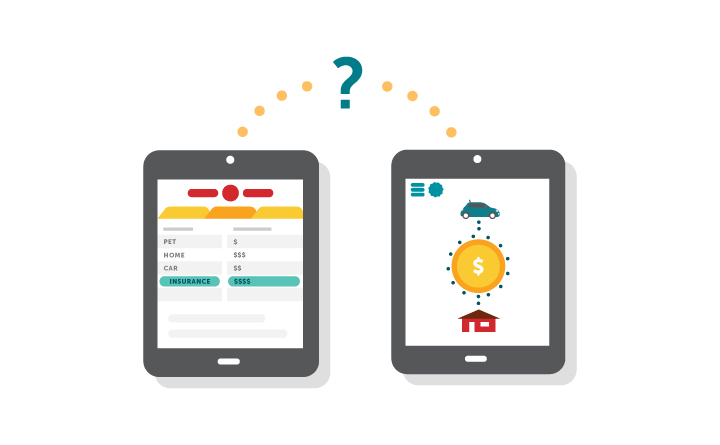

10. Resolution: Review My Insurance Costs and Coverage

Action: Add Up Costs and Coverage, Then Comparison Shop

Review your current insurance, including your coverage, premiums and deductions and shop around to see if there's a better deal. Depending on your situation, this might include:

- Auto insurance

- Homeowners insurance

- Renters insurance

- Small business insurance

- Health insurance

- Life insurance

Set aside time for online research or call an independent agent (who has access to multiple plans) to investigate alternatives. You may find that you are over-insured, underinsured or are paying too much for what you're getting in return.

For example, you may be able to reduce your auto insurance premium by increasing your deductible. Just make sure you are prepared to pay a larger out-of-pocket expense if you have a claim. You can also inquire about other discounts, such as a lower cost for paying your premium in one lump sum instead of monthly, a safe driver discount, or pay-per-mile discounts that charge based on the number of miles driven.

With any independent agents you engage with, make sure to take steps to verify their credentials, research their public reviews and understand how they're compensated. For example, do they charge a fee, or are they paid by insurance providers?

11. Resolution: Increase the Security of My Financial Accounts

Action: Update Passwords on Financial Accounts

Your hard-earned cash deserves a safe home. Fraud, scams and hacks can all drain your bank accounts.

Review your logins and change passwords if you haven't done so during the last six months. Be sure not to share logins and passwords with others, and stay ahead of any text scams and phishing attempts.

Final Word: Plan for Next Year

Once you've taken steps to follow through on your financial New Year's resolutions, it's time to celebrate — then start the planning process for next year. Note anything you postponed or procrastinated on this year and make sure to include them in your future planning.

Also note items you found difficult to achieve: What were the barriers, and what might you do differently next year?

For example, you might note that you rushed to make year-end donations and struggled to come up with the funds this year. Moving forward, you can set up automatic, monthly donations and alleviate last-minute stress.

With a little practice and consistent effort, you'll have stronger money muscles and come closer to achieving your goals.

The above article is intended to provide generalized financial information designed to educate a broad segment of the public; it does not give personalized financial, tax, investment, legal, or other business and professional advice. Before taking any action, you should always seek the assistance of a professional who knows your particular situation when making financial, legal, tax, investment, or any other business and professional decisions that affect you and/or your business.

Related Content

Stacey Black

(She/Her/Hers)

BECU Lead Financial Educator